20

Oct

How to setup xreg argument in autoarima in R. Hi I am trying to understand exactly what xreg does in arima.

R auto arima xreg. Autoarimadiffvisits xreg xreg is asking autoarima to fit an ARIMA model on 48 observations using external regressors with nrow of 49. Endgroup Jubbles Jan 6 16 at 1908 begingroup Jubbles i got the answer a while ago. There are 2 ways to handle this.

Autoarimadiffdiffvisits xregdiffdiffxreg 2nd method. I am working on project to forecast sales of stores to learn forecastingTill now I have successfully used simple autoArima function for forecastingBut to make these forecast more accurate I can make use of covariatesI have defined covariates like holidays promotion which affect on sales of store using xreg operator with the help of this post. How to setup xreg argument in autoarima in R.

The R function Arima will fit a regression model with ARIMA errors if the argument xreg is used. The order argument specifies the order of the ARIMA error model. If differencing is specified then the differencing is applied to all variables in the regression model before the model is estimated.

For example the R command. 0 Verwenden der Kombinationsprognose autoarima 3 Prognose Zeitreihe mit R Vorhersage Paket. 1 Prognose Mit dem xreg-Parameter in forecastgts mit mehreren externen Variablen mit unterschiedlichen Werten pro Zeitreihe hts-Paket 1 Zeitreihenvorhersage in R.

21 Zeitreihe Forecasting mit bekannten Großaufträge zu tun. Arima_reg is a way to generate a specification of an ARIMA model before fitting and allows the model to be created using different packages. Currently the only package is forecast.

Xreg is rank deficient but I should not get rid of columns with zeros because it was obtained after one-hot encoding. So I was wondering how to resolve this. In order to explain in detail.

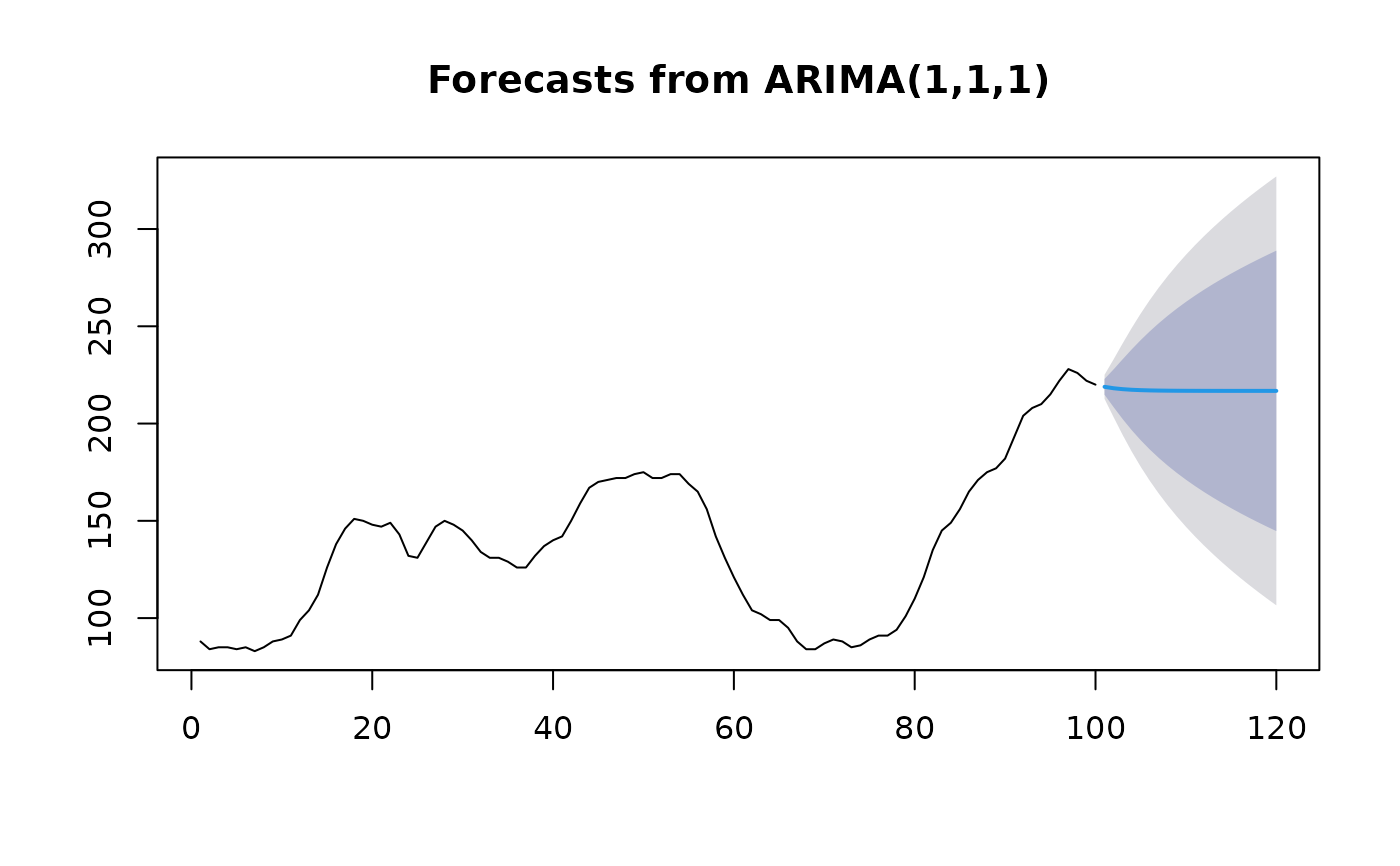

Fit best ARIMA model to univariate time series Description. Returns best ARIMA model according to either AIC AICc or BIC value. The function conducts a search over possible model within the order constraints provided.

Using xreg suggests that you have external exogenous variables. In this a regression model is fitted to the external variables with ARIMA errors. When forecasting you need to provide future values of these external variables.

In practice these are often forecasts or could be known. Fitting an autoarima model in R using the Forecast package fit_basic1. Now lets look at the residuals of the model.

Passen Sie das Modell mit der arima-Funktion in die Basis R ein. Diese Funktion kann ARMAX-Modelle mithilfe des xreg Arguments verarbeiten. Probieren Sie die Funktionen Arima und autoarima im Vorhersagepaket aus.

Autoarima ist nett weil es automatisch gute Parameter für Ihr Arima-Modell. Perhaps LEADIND would also be helpful as a regressor in the seasonal ARIMA model we subsequently fitted to auto sales. To test this hypothesis the RESIDUALS from the ARIMA011x011 model fitted to AUTOSALE were saved.

Their cross-correlations with DIFFLOGLEADIND plotted in the Descriptive Methods procedure are as follows. Hi I am trying to understand exactly what xreg does in arima. The documentation for xreg saysxreg Optionally a vector or matrix of external regressors which must have the same number of rows as x What does this mean with regard to the action of xreg in arima.

Apparently somehow xreg made the following two arima fit equivalent in R. Arimax orderc111 xreg1lengthx is the same.

Previous post

Raag kafi songs listNext post

Queensland areas affected flood